If your 2022 refund or balance due turns out not to be the desired amount, you may want to consider adjusting your withholding based on your projected tax for 2023. If you need assistance, please call this office.

W-9 Collection – If you are operating a business, then you are required to issue a Form 1099-NEC to each service provider to which you have paid at least $600 during a given year. It is a good practice to collect a completed W-9 form from every service provider (even if you are paying less than $600), as you may use that provider again later in the year and may have difficulty getting a W-9 after the fact—especially from providers that do not plan to report all of their income for the year.

Estimated Tax Payments – If you are self-employed, then you prepay each year’s taxes in quarterly estimated payments by sending 1040-ES payment vouchers or making electronic payments. For the 2023 tax year, the first three payments are due on April 18, June 15, and September 15, 2023, and the final payment is due on January 16, 2024. Generally, these payments are based on the prior year’s taxable income; if you expect any significant changes in either income or deductions relative to the previous year, please contact this office for help in adjusting your payments accordingly.

Charitable Contributions – If you marginally itemize your deductions, then you can employ the bunching strategy, which involves taking the standard deduction one year but itemizing your deductions in the next. However, you must make this decision early in the year so that you can make two years’ worth of charitable contributions in the bunching year.

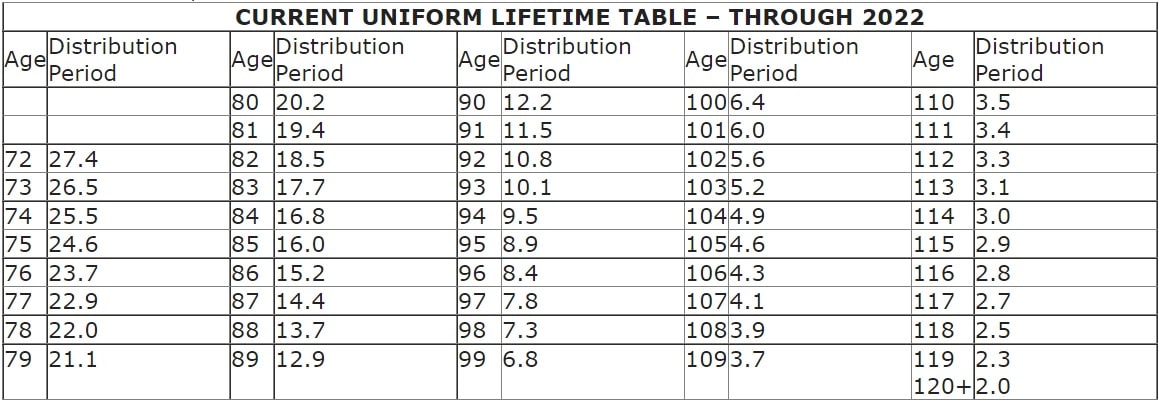

Required Minimum Distributions – Each year, if you are 73 (a recent law change increased it from 72 in 2022) or older, you must take a required minimum distribution from each of your retirement accounts or face a substantial penalty. By taking this distribution early in the year, you can ensure that you do not forget and accidentally subject yourself to penalties.

Gifting – If you are looking to reduce your estate-tax exposure or if you just want to give some money to family members, know that each year, you can gift up to an inflation-adjusted amount, which for 2023 is $17,000, to each of an unlimited number of beneficiaries without affecting your lifetime estate-tax exclusion amount or paying a gift tax.

Retirement-Plan Contributions – Review your retirement-plan contributions to determine whether you can afford to increase your contribution amounts and to make sure that you are taking full advantage of your employer’s contributions to the plan.

Beneficiaries – Marriages, divorces, births, deaths, and even family clashes all affect whom you include as a beneficiary. It is good practice to periodically review not just your will or trust but also your retirement plans, insurance policies, property holdings, and other investments to be sure that your beneficiary designations are up to date.

Reasonable Compensation – With the advent a few years ago of the 20% pass-through deduction, which is available to most businesses other than C-corporations, the issue of reasonable compensation took on new importance, particularly for shareholders of S corporations. This has been a contentious issue in the past, as it has allowed shareholders who are not just investors but who are actually working in the business to take a minimum salary (or no salary at all) so that all their income passed through the K-1 as investment income. This strategy allows such shareholders and the S corporation to avoid payroll taxes on income that should be treated as W-2 compensation. A number of issues factor into a discussion of reasonable compensation, including comparisons to others working in similar businesses and to employees within the same business, as well as the cost of living in the business’s locale. This is a subjective amount, and it generally must be determined by a firm that specializes in making such determinations.

Business-Vehicle Mileage – Generally, vehicles with business use also have some amount of nondeductible personal use in a given year. It is always a good practice to record a vehicle’s mileage at the beginning and at the end of each year so as to determine its total mileage for that year. The total mileage figure is then used when prorating the personal- and business-use expenses related to that vehicle.

College-Tuition Plans – Contribute to your child’s Section 529 plan as soon as possible; the funds begin accumulating earnings as soon as they are in the account, which is important because the student will likely begin using that money at age 18 or 19.

Only a few of the tax-related actions that you take during a year will benefit yourself or others. The most important of these actions is keeping timely and accurate tax records; for businesses in particular, this is of the utmost importance. Those who have well-documented income and expense records generally come out on top when the IRS challenges them.

If you have any questions related to your taxes or if would like an appointment for tax projections or tax planning, please contact our office.